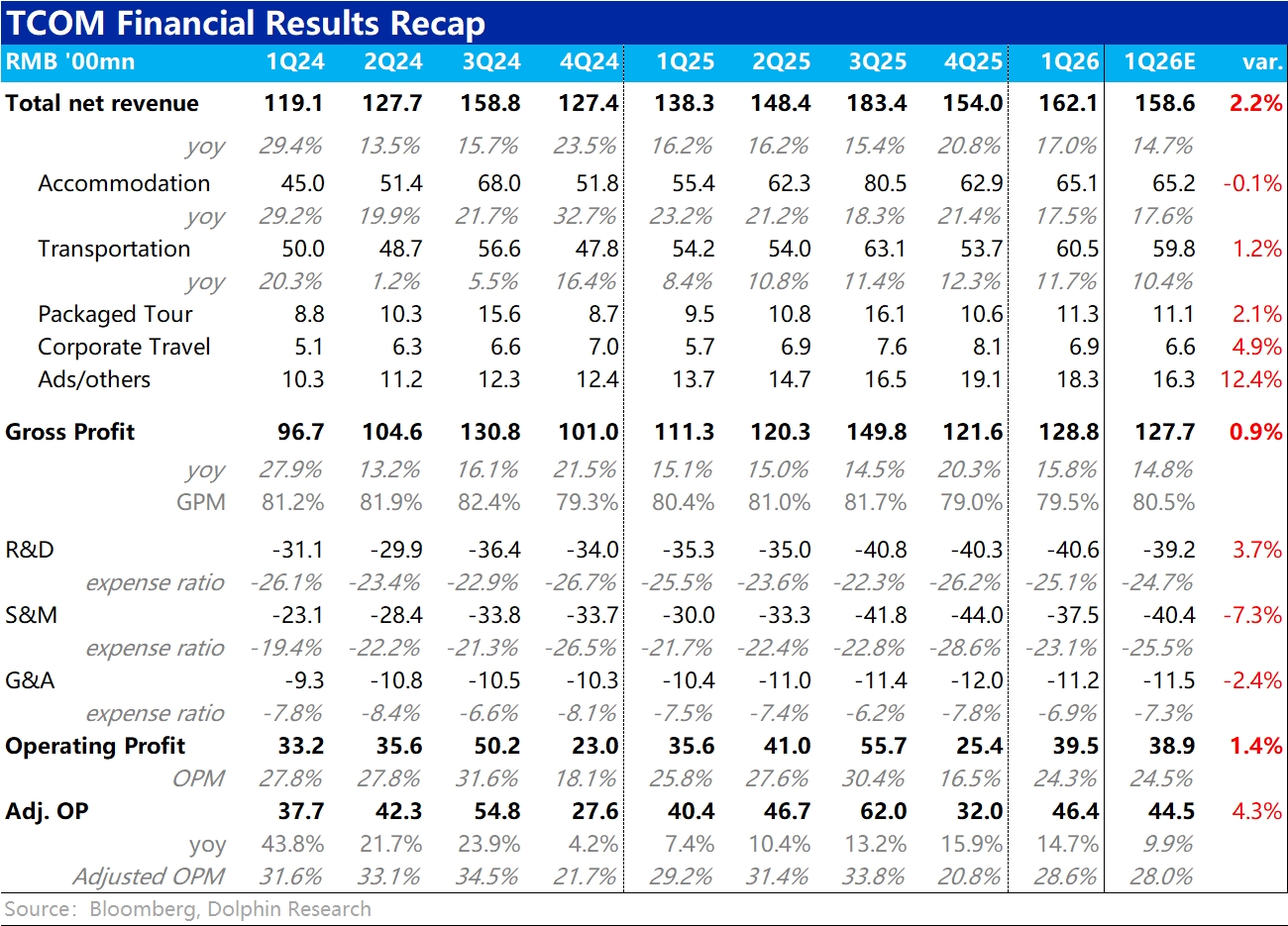

Trip.com 1Q26 First Take: likely under regulatory overhang, the company finally released its delayed Q1 results. Overall, three takeaways stand out: 1) results remained solid with healthy revenue growth and profits; 2) the regulatory review is ongoing, with final remediation and any penalties still undisclosed; 3) management guided next-quarter revenue growth to just 3%–8%, with profitability to be hit as well, a post-pandemic low that signals regulatory impact starting to bite.

Revenue grew ~17% YoY, a modest slowdown from the 20%+ pace in the prior quarter but above the 15% street view. GPM fell ~90bps YoY, but expenses, especially marketing, came in well below expectations, lifting earnings. Adj. OP exceeded RMB 4.6bn (+10% YoY), beating the RMB 4.45bn estimate.

Leaving the beat aside, GPM still contracted ~90bps YoY while total opex rose 18%, outpacing revenue. This suggests an investment phase, pressuring margins (OPM narrowed 120bps YoY) and leading to limited profit conversion from top-line growth.

While current results are decent, the key issue is the very weak guide for next quarter. Management cited two drivers: the U.S.-Iran conflict and higher oil prices weighing on travel in affected regions, and voluntary operating adjustments to comply with regulators.

As the Middle East is not Trip.com's core overseas market, and OTA peers have actually traded well recently on World Cup tailwinds, Dolphin Research believes the U.S.-Iran conflict is not the primary factor. Domestic regulatory impact likely matters more.

Details in the release are limited, so watch the earnings call and subsequent small-group meetings for updates on the review and potential business impact. $Trip.com(TCOM.US) $TRIP.COM-S(09961.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.