I spent some time carefully studying SK Hynix's earnings report today.

I converted the data into US dollars:

Q1 revenue was $35.5 billion (up 3x year-over-year), operating profit was $25.4 billion (up 5x year-over-year, doubling quarter-over-quarter), with an operating profit margin of 72% hitting a record high. Both revenue and profit were slightly below expectations.

Currently, the capital market places more emphasis on the direction of the profit margin than on the revenue figure.

An interesting phenomenon in the memory sector is that at the peak of the memory cycle (when profits are highest), stocks have extremely low forward P/E ratios. For example, Hynix is around 4–8x, and Micron is also very low now, under 10x, which looks very attractive to buy, with significant upside potential.

However, there's a market logic for valuing and pricing memory stocks: the higher the profits, the less the market believes they can be sustained. What the market cares more about is whether memory companies can sustain a profit surge and have a steady stream of growth expectations and long-term orders for 5-10 years.

Therefore, the market gives TSMC and NVIDIA a P/E of over 20x but is unwilling to give memory stocks that multiple. Moreover, TSM is essentially a monopoly, but these memory companies still compete with each other on some products; there isn't a single giant that completely monopolizes the entire memory market. This is also related to pricing.

Next week, besides the explosive data (already priced in) for SNDK, the key focus will be on its future business outlook. Also, the optimistic sentiment and strong guidance provided by management. I checked the options chain; the current IV is 117%, indicating high volatility. There could be a 15-20% swing. Therefore, management cannot have any conservative wording during the conference call. If it appears, it will be magnified multiple times, causing a stock price pullback, like a sudden drop of over $100. If everything goes smoothly, is explosive, and optimistic, with a good outlook lasting for several years, then a sudden surge is also very normal.

Only when the earnings reports of these leading stocks show high expectations and a strong business outlook for several years ahead can the market break through the previous bias of cyclical stock pricing and truly give memory stocks a valuation logic similar to TSM. If the earnings report can fully demonstrate these factors, then the so-called super memory cycle still has great potential ahead.

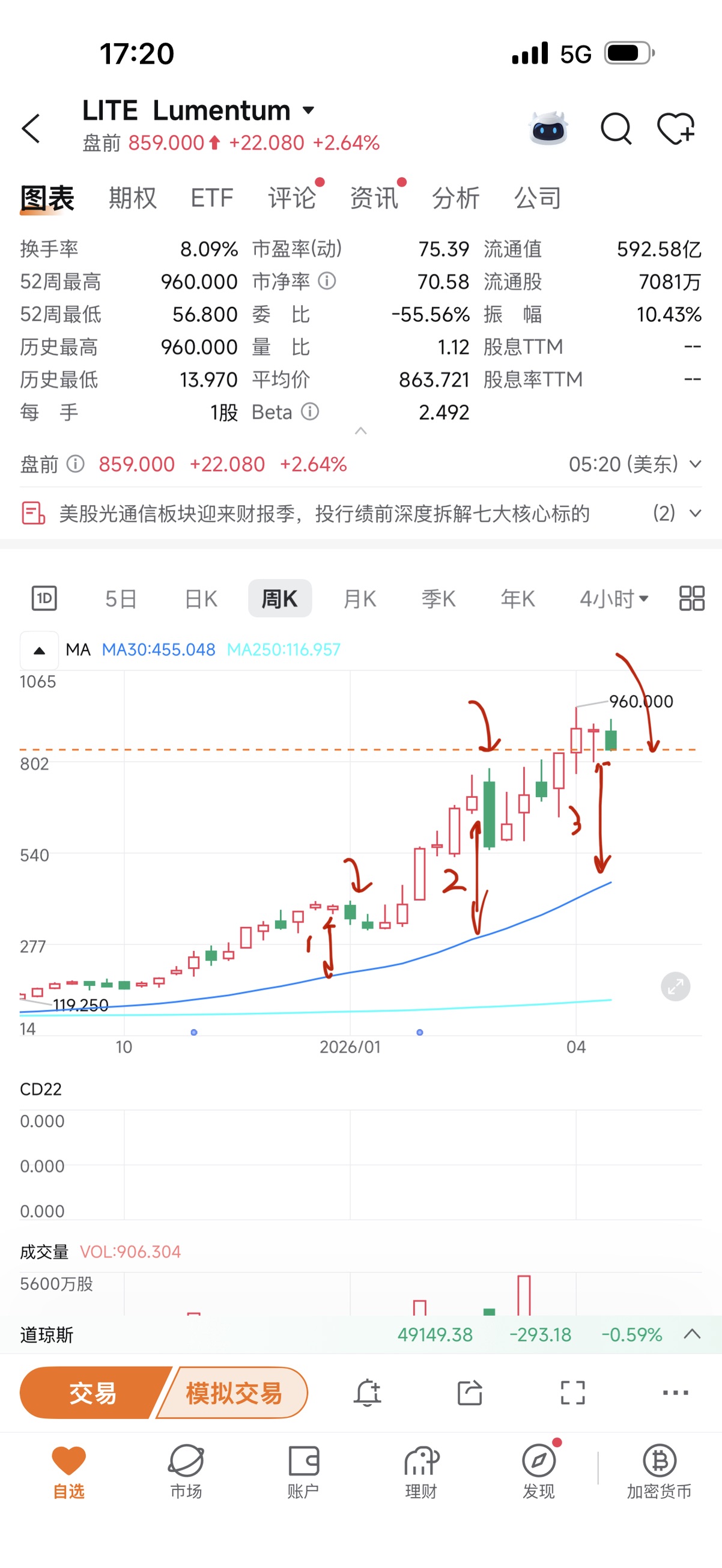

Discussing the trends of storage stock SNDK and optical communication stock LITE through NVDA's weekly K-charts over the past five years.

Fundamental Analysis

The community has detailed analyses on SNDK and LITE. In short, it's a super cycle for storage and optical communication, with shortages expected for at least two to three years.

Revenue and profits are experiencing explosive growth.

Since its spin-off from WD in February 2025, SNDK's stock price has surged 650%. NAND shortages and rising prices, coupled with supply capacity far lagging behind the demand from AI data centers, have caused its gross margin to skyrocket to 51.1% in the short term. HBF and SK Hynix are jointly developing, with mass production possible by 2027.

The end-of-month earnings report will reveal the company's hyper-growth and next-quarter guidance data, which we'll analyze later.

The risk lies in the stock price's excessive short-term gains, with a P/E of 67 and YTD up 132%. If the positive earnings report cannot match the high premium priced in by the market, a pullback is likely. The market has already priced in these explosive data points.

LITE's production capacity is fully booked for the next three years, leaving little to research. The market has already moved on to hype stocks like CRDO and POET. A P/E of 39 is actually okay. However, its high dependence on a few major clients is a risk.

Technical Analysis

NVDA took three years to rise from 39 to 200+, with ample adjustments and position exchanges in between. In contrast, SNDK and LITE have risen too quickly without experiencing significant declines. Despite the super cycle and strong fundamental support, their rapid ascent from the bottom with little adjustment, based on our over-a-decade of market-watching experience, suggests a significant correction is likely in the near term.

I've marked several arrows. All three charts are weekly charts. Whenever the candle's bottom deviates too much (steeper) from the MA30 weekly moving average, it's prone to close negative in the following weeks.

I'm not calling a top because super cycles don't have clear tops. NVDA is still growing rapidly. Google, Microsoft, Amazon, and Meta's combined capital expenditure this year is over 600 billion. How bad can it be for the shovel sellers?

Looking at the chart, this big red candle will likely be hard to escape. It's just a matter of a few weeks earlier or later.

Long-term investors can ignore it. Short-term traders just need to be aware of the risks. Actually, I don't recommend short-term trading with such stocks; there's not much money to be made. My own lesson is missing out on hundreds of thousands with 5000 shares of NVDA. Once the price goes up, it's not easy to come back down.

I will re-enter after a pullback when the weekly chart reaches support. We'll talk about the lines later.

Chip stocks are also starting to spread from the hype around NVDA/AVGO to MRVL/AMD.

Additionally, BTC 75K has clearly become a support level. If it stabilizes above 78K, the highest target is 85K. I'm still holding my MSTR CALL.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.