PDD 4Q25 First Take: As Dolphin Research has noted, PDD has stayed out of the food-delivery land grab and is not chasing AI hype, emerging as the most focused, pure-play, value-oriented retailer in e-commerce. This was again the steadiest print among peers, with most metrics largely in line with the Street.

Key signals: domestic operations were broadly stable, and PDD was less affected as state subsidies faded. Temu’s growth was stronger than expected, specifically:

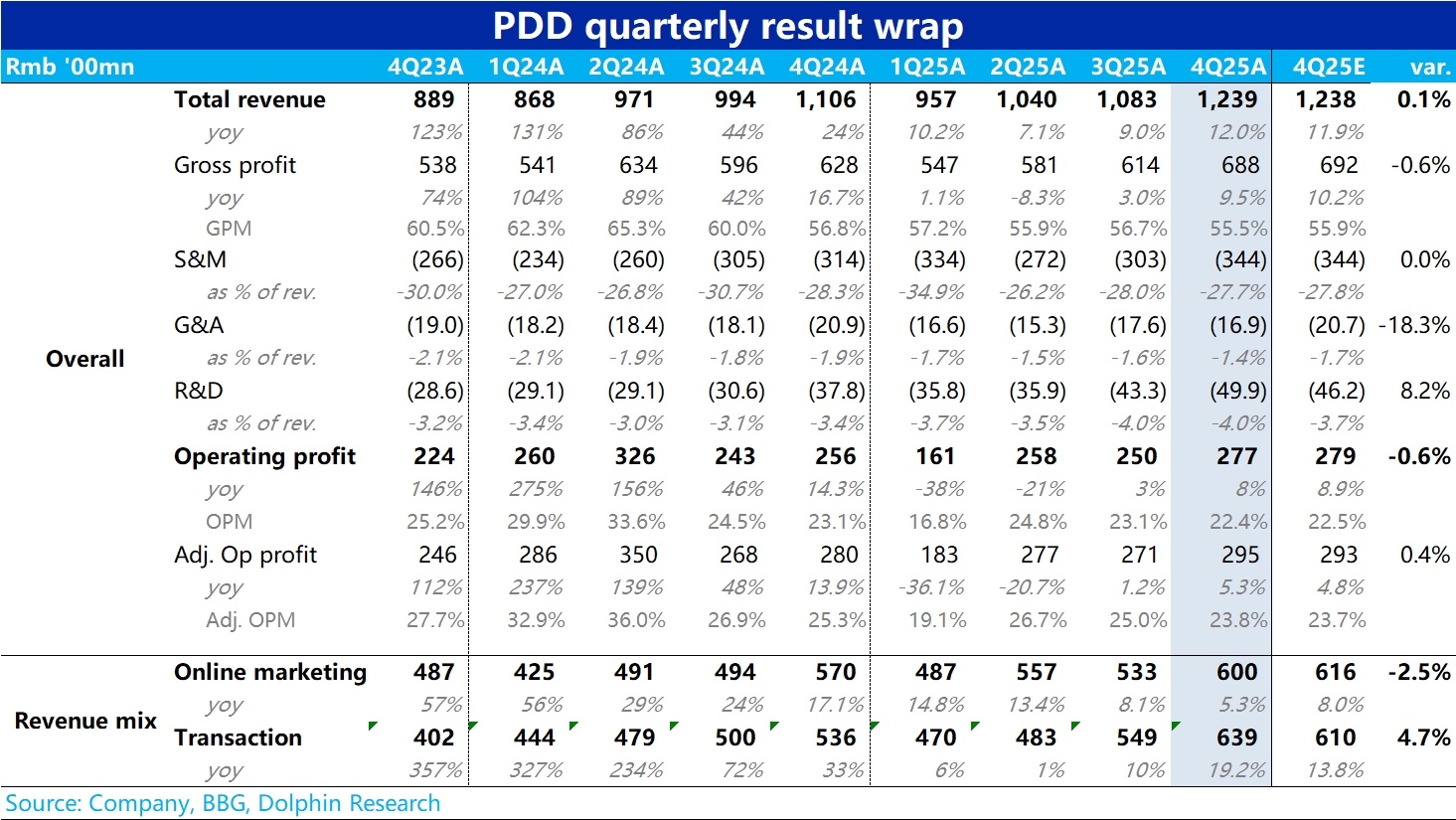

1) Total revenue rose 12% YoY, fully in line. By line item, online marketing revenue grew 5.3% YoY, below Bloomberg consensus of 8%; even GS was at 6%, so it still lagged.

Referencing recent prints from JD and Alibaba, this likely reflects a sluggish 4Q e-commerce backdrop. QoQ, growth eased only from 8% to 5%, suggesting the fade of state subsidies was a marginal positive for PDD.

2) The upside came from transaction services revenue, up 19% YoY and clearly ahead of the Street. Given weak domestic trends this quarter, most of the beat likely came from Temu. With Meituan largely exiting community retail, Duoduo Maicai may have also contributed.

3) GPM was a touch below expectations, likely a mix headwind as Temu scaled and its weight increased. The gap is immaterial. The largest expense, sales & marketing, was RMB 34.4bn (+9.6% YoY), also in line.

Notably, sales expense growth accelerated vs. the prior two quarters. Dolphin Research believes that as the impact of state subsidies faded, marketing spend on the domestic core app likely did not rise much. That implies heavier Temu investment, consistent with its upside this quarter.

4) Lastly, G&A and R&D moved in opposite directions, largely offsetting. The former reflects higher productivity, the latter ongoing AI investments. OP was broadly in line; on an adj. basis, up ~5% YoY. $PDD(PDD.US) $PDD 2X Long ETF(KPDD.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.