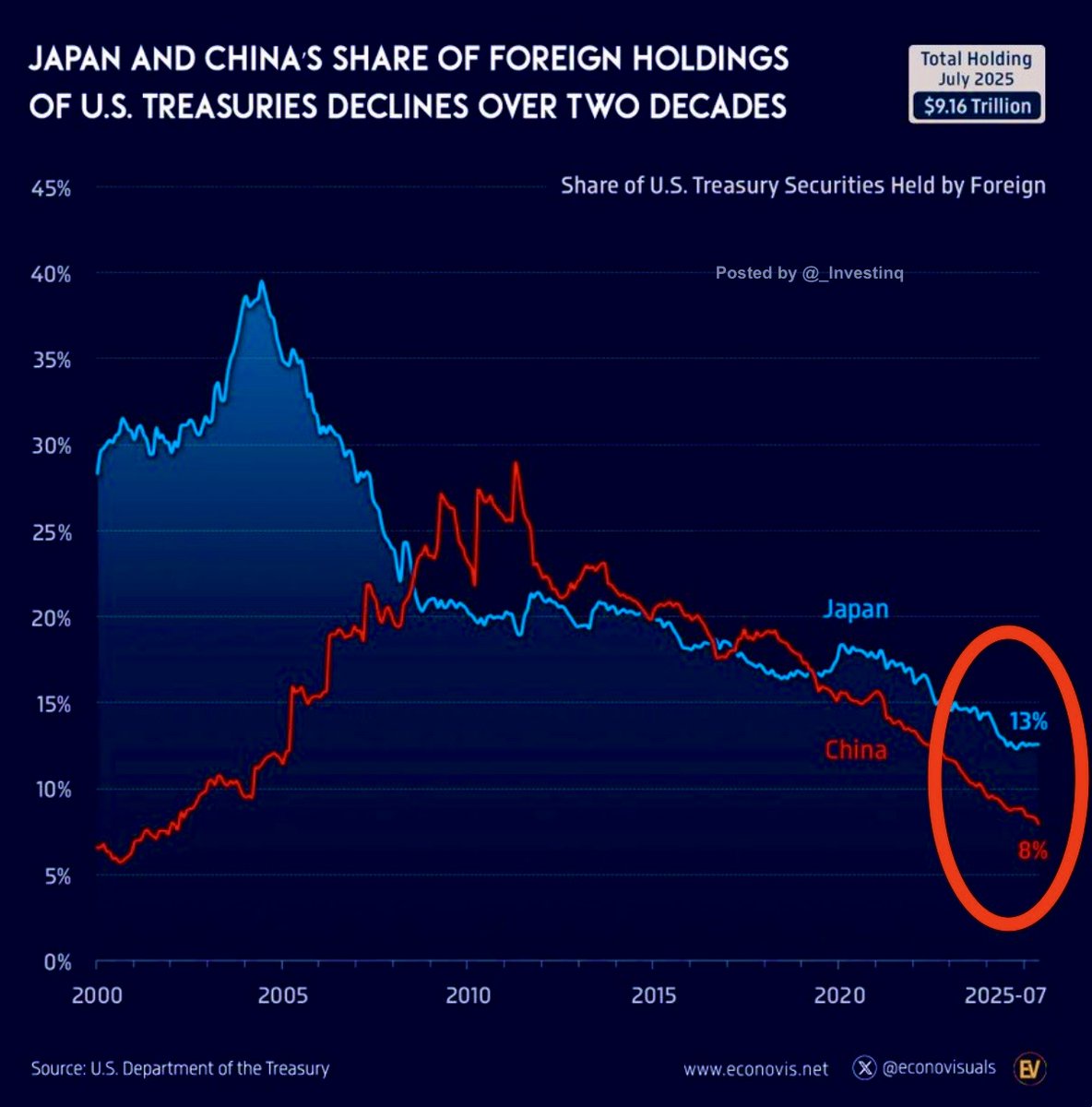

Back in the early 2000s, Japan and China were basically the backbone of foreign demand for U.S. Treasuries. Japan once held close to 40% of all foreign-owned Treasuries, and China reached about 29% at its peak but as of mid 2025, Japan’s share is down to 13% and China’s to 8%. Together, that’s only around one fifth of what foreign investors hold down from nearly two-thirds at the peak. That’s a huge drop that says a lot about how global finance is changing

For Japan, the main reason has been economic. The yen fell to its weakest level in decades around 160 per dollar so Japanese authorities sold Treasuries to buy yen and support their currency. Japanese investors are also finding better returns at home now that local interest rates have started rising after decades of near-zero policy. The Bank of Japan’s subtle policy shift made Japanese government bonds more appealing, so money has been flowing back home.China’s case is different. Its decline is driven by strategy and caution. After years of tension with Washington from trade wars to technology bans China has been slowly cutting exposure to U.S. assets. But instead of dumping Treasuries overnight (which would crash their value and hurt China’s own portfolio), Beijing has been diversifying. It’s been building systems to trade in yuan investing in gold, and promoting the Belt and Road Initiative to reduce reliance on the dollar system. The goal isn’t to attack, the U.S. financially, it’s to make sure China isn’t overly dependent on a financial system America controls.The bigger story here is what’s happening underneath, the world is gradually shifting away from financing U.S. deficits. Foreign ownership of U.S. debt was more than 50% during the 2008 crisis, it’s now under 30%. That doesn’t mean the dollar is dying, but it does mean fewer countries want to keep all their savings in Treasuries. Economists call this “stealth de-dollarization”, a slow move away from dollar assets without a big crash.There are ripple effects. When foreign governments step back, private investors have to fill the gap and private investors only buy Treasuries if the yields are high enough to justify the risk. That helps explain why long-term interest rates have been volatile: there’s more debt to absorb, but fewer buyers willing to hold it cheaply. Every time a big holder like China or Japan sells, yields often spike because the U.S. has to pay more to attract buyers.Japan and China haven’t stopped buying Treasuries altogether, they’re just rebalancing. Japan has been putting more into European bonds, while China is experimenting with regional systems that let countries settle trade in yuan instead of dollars. But both remain tied to U.S. stability, they can’t risk a crash in the Treasury market because that would hurt everyone, including them.So what’s really happening here is the slow end of a financial era. For decades, Asian surplus countries financed America’s deficits in exchange for stability and export demand. Now, as geopolitics shift and domestic priorities rise, they’re stepping back. The U.S. will have to rely more on domestic buyers or pay higher yields to keep the world lending. It’s not an immediate crisis but it’s a clear signal that global finance is becoming more fragmented, and that the dollar’s dominance, while still strong, is gradually being tested.Source: StockMarket.News

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.