ATFX:USDJPY fell sharply, with the market price breaking below the 161 level

ATFX Market Review: Japanese Finance Minister Kato Tsuyoko stated this morning that they are ready to take appropriate action on the yen exchange rate at any time and are maintaining close communication with the United States. The Japanese Ministry of Finance had already indicated its intention to intervene in the yen exchange rate back in May of this year, with Kato Tsuyoko's wording at the time being "will take bold action to maintain exchange rate stability." The Japanese Ministry of Finance used a large amount of funds to sell dollars and buy yen in an attempt to suppress the rise of USDJPY, but judging from the actual market movements, the effect has been minimal.

Last night, the U.S. Bureau of Labor Statistics released the June non-farm payroll report, which showed that the number of new non-farm jobs plummeted from 129,000 to 57,000, far below the expected 110,000. The unexpectedly weak data shook market confidence in the Federal Reserve's interest rate hikes in the second half of the year, causing the U.S. Dollar Index to tumble and USDJPY to also experience sharp fluctuations.

ATFX Chart▲

Within one minute of the data release, USDJPY fell from 161.51 to 160.93, a drop of 54 basis points. In the following minutes, the price dipped further to 160.62, with a cumulative maximum decline of 89 basis points, far exceeding past performances. From 14:33 to 14:34 Beijing time today, USDJPY experienced another sharp decline, with the market price falling from the opening of 161.00 to 160.47, a drop of 53 basis points. It is evident that the first round of decline was a chain reaction caused by the unexpectedly weak U.S. non-farm payroll report, while the second round of decline was likely a yen exchange rate intervention measure conducted by the Japanese Ministry of Finance taking advantage of the situation.

Comparing the movements of the two rounds of yen appreciation, the impact of the weak U.S. labor market is clearly greater than the intervention policies of the Japanese Ministry of Finance. This means that the long-term trend of USDJPY may not depend on the control of the Japanese Ministry of Finance, but rather on the monetary policy expectations of the Federal Reserve and the actual movements of the U.S. Dollar Index.

ATFX Chart▲

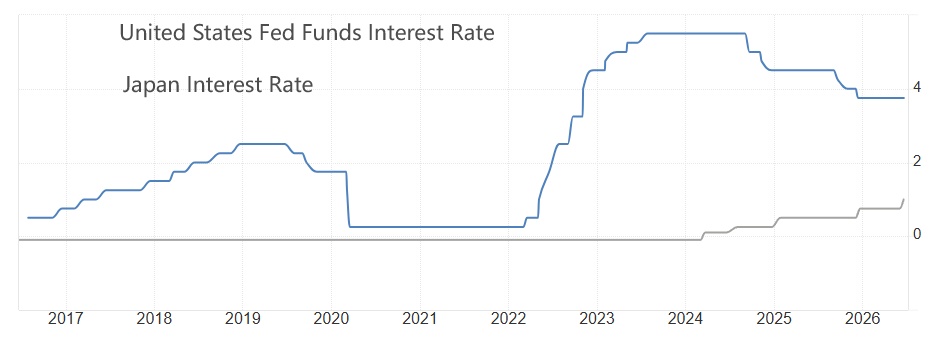

From March 2024 to the present, the Bank of Japan has raised interest rates five times, increasing the rate from negative to 1%. The Federal Reserve has cut interest rates three times over the past period, with a cumulative reduction of 75 basis points, and the upper limit of the benchmark rate is 3.75%. From the perspective of monetary policy direction, the Bank of Japan is raising rates while the Federal Reserve is cutting rates, narrowing the Japan-U.S. interest rate differential, which is positive for the yen's value. However, during the process of narrowing the Japan-U.S. interest rate differential, USDJPY not only did not fall but instead led the gains among other major currency pairs. A possible reason is that the yen is a funding and safe-haven currency. Even after several rounds of rate hikes, its absolute interest rate remains relatively low, unable to effectively drive profit-seeking capital to shift from the U.S. dollar to the yen.

For the analysis of USDJPY's future trend, it is recommended to base it on the movements of the U.S. Dollar Index, appropriately reduce the impact of the Bank of Japan's monetary policy and the Japanese Ministry of Finance's control on the exchange rate, and respect the established trend of the yen's continuous depreciation against the U.S. dollar over the years and the objective functional status of the yen as a funding currency.

ATFX Risk Warning, Disclaimer, Special Notice: The market carries risks, and investment requires caution. The above content only represents the personal views of the analyst and does not constitute any operational advice. Please do not consider this report as the sole reference. At different times, the analyst's views may change, and updated content will not be notified separately.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.