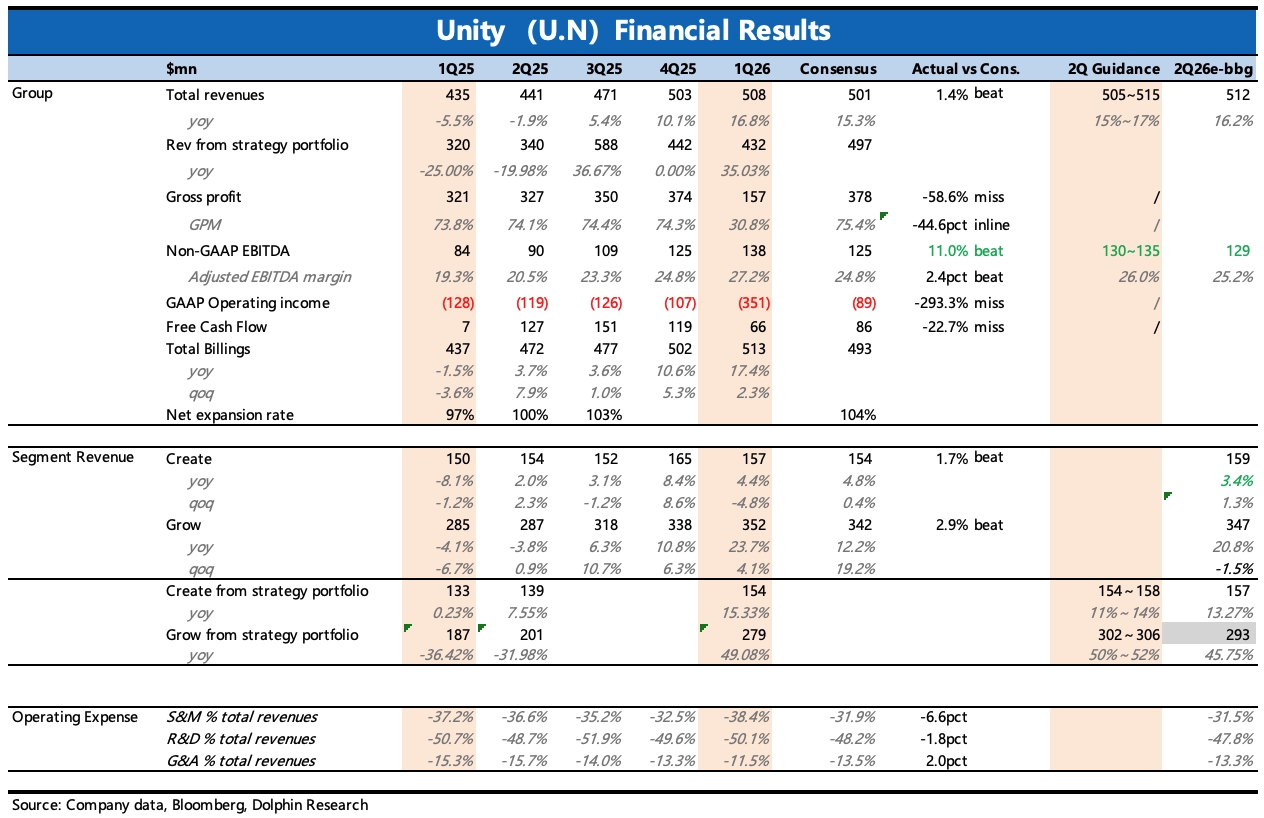

Unity 1Q26 First Take: Unity pre-announced 1Q results in late Mar and disclosed plans to separate IronSource and Supersonic; background in our prior note (Unity Q1 业绩预告点评). Revenue came in slightly above the pre-announced range.Excluding scope changes, EBITDA beat as tighter cost control following portfolio refocus drove operating efficiency.

Also supportive for sentiment: management guided Q2 ads revenue above Street. Engine revenue is in line as the early-year price hike underpins organic growth.

Note BBG consensus has a lag: several models were submitted before Mar, so the Strategic segment in some estimates still includes IronSource and Supersonic. That makes the Q2 Strategic Grow revenue guide of $300mn look below the $340mn consensus.

Adjusting consensus to exclude IronSource and Supersonic, the market was at Approx. $290mn for Q2 Strategic Grow; the $300mn guide is slightly above, implying Unity Ads ~50% YoY.We expect Q2 to benefit from the D28 algorithm driving deeper client penetration and data integration with the Runtime engine. With competition intensifying at the margin, management’s view on the longer-term vector trend is key; watch for more detailed KPIs on the call. $Unity Software(U.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.