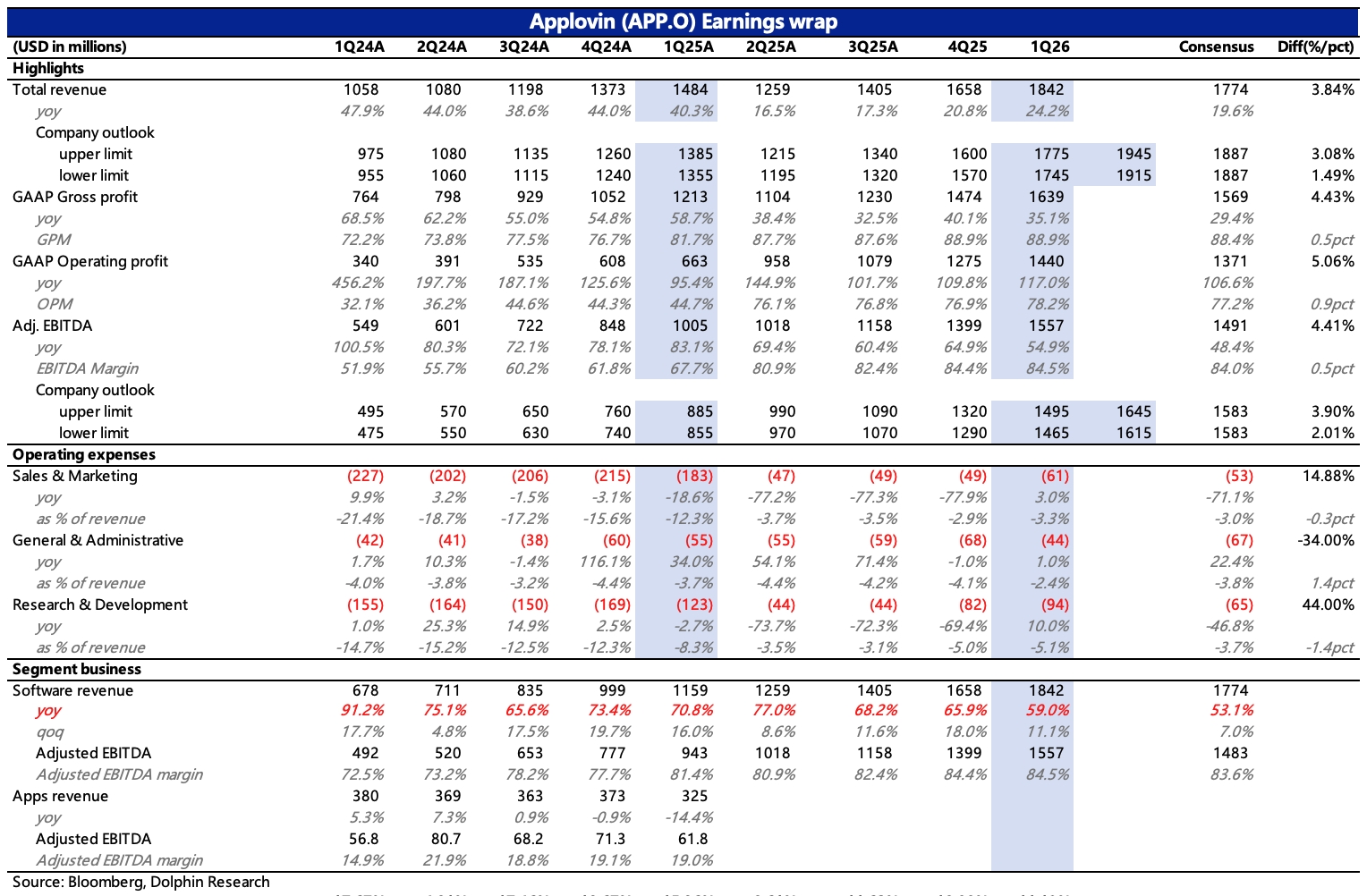

APP 1Q26 First Take: Overall results were a small beat.

Organic growth was +59% in Q1, with Q2 guided at +55%, supported by resilient gaming ad share and incremental e-comm ads. Setting guidance aside, Dolphin Research sees both upside surprises and minor blemishes.

(1) The positive: margin stability. As competition intensifies, gaining share likely requires more client-facing incentives and investment in new marketing tools, which could pressure margins.

Against this backdrop, AppLovin’s high margins had downside risk.

In reality, Q1 GPM was stable, while OPM rose 100bps QoQ to 78%, and Q2 guidance does not point to weaker margins.

Client-interaction-related sales expenses increased, but tighter G&A helped lift overall operating efficiency.

(2) The blemish: slower growth. Q1 organic growth decelerated from Q4’s 66%, with QoQ growth of 11%.

That beat the company’s mid- to long-term target of ~5% QoQ, but still trailed 1Q25’s 16%, signaling moderation.

Set against AppLovin’s push into e-comm ad TAM expansion, the signal may be less than stellar.

Dolphin estimates that assuming gaming and other ads grew ~30% organically, e-comm ads likely reached $400mn+ in Q1, up about 250% YoY from an early-stage base.

Triangulating Q1 with channel checks, AppLovin’s competitive edge remains evident, though rivals’ campaign performance may still be in optimization.

With mobile ads expanding as app store rev-share takes decline, we expect AppLovin’s high growth to persist in the near to mid term.

With shares under pressure in Q1, the company doubled buybacks vs. Q4 to $1bn.

It repurchased 2.2mn shares at an avg. $450/share. $AppLovin(APP.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.