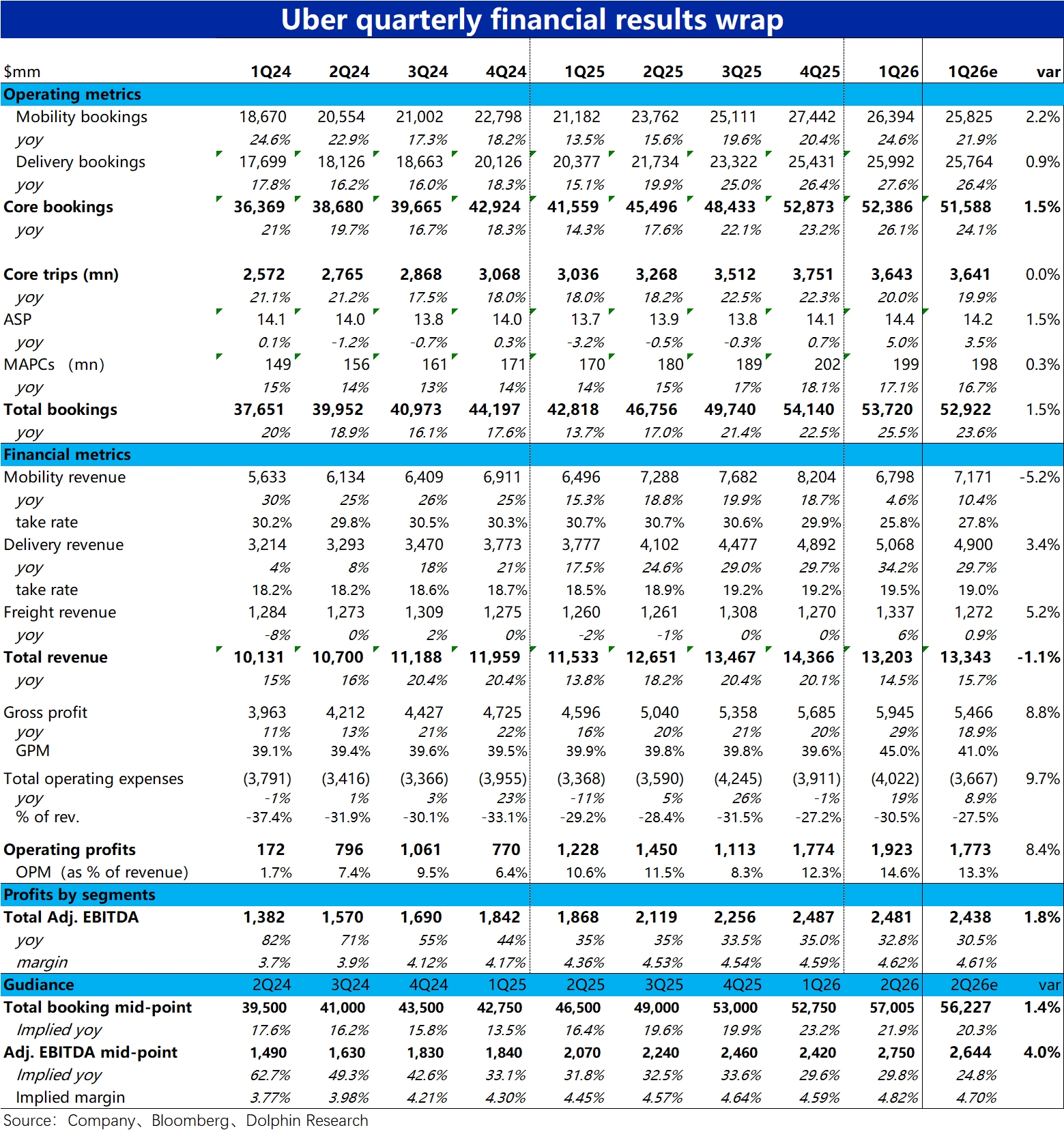

Uber 1Q26 First Take: The ride-hailing leader delivered another steady print, with Gross Bookings and adj. EBITDA both slightly ahead of Street expectations. Growth momentum remained broadly in line with last quarter at elevated levels, while margins continued to expand. The bigger highlight was a stronger next-quarter guide, suggesting bookings may keep accelerating with a wider margin uptick.

In detail:

1) Core businesses (Mobility + Delivery) saw Gross Bookings up 26% YoY, a clear step-up from 23% last quarter and above consensus. Actual trips rose 20% YoY vs. 22% in the prior quarter, as average order value increased by nearly 5% YoY, well above recent trends. This implies underlying growth was similar to last quarter, with pricing helped by a notable FX tailwind.

2) By segment, Mobility GB growth at cc was 20%, an acceleration of 1ppt vs. last quarter. Delivery cc growth moderated to 23% from last quarter’s recent peak of 26%.

3) Revenue trends diverged by segment. With oil prices rising amid the Middle East conflict, the company and peers provided fuel subsidies to drivers that were recorded as contra-revenue, leaving Mobility revenue up just 5% YoY and well below expectations, implying subsidies likely exceeded $1 bn. Conversely, despite slower Delivery GB growth, a higher monetization rate drove a sharp acceleration in reported revenue growth, while cc growth was broadly in line with last quarter.

4) On profitability, management shifted its primary metric from adj. EBITDA to adj. operating profit to reduce adjustment effects. On the new basis, Mobility adj. OPM expanded by 20bps YoY, suggesting insurance cost tailwinds outweighed the impact of fuel subsidies. Delivery margin improved by 40bps, consistent with the higher monetization trend.

5) For next quarter, the company guides Gross Bookings of $56.25–57.8 bn, with the low end in line with Street. This implies cc growth of 18–22%; at the high end, growth would tick up modestly vs. 21% this quarter.

Adj. EBITDA guidance is $2.7–2.8 bn, with the low end already above the $2.65 bn consensus. At the midpoint, implied margin is 4.8% vs. 4.5% a year ago, indicating further expansion. $Uber Tech(UBER.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.