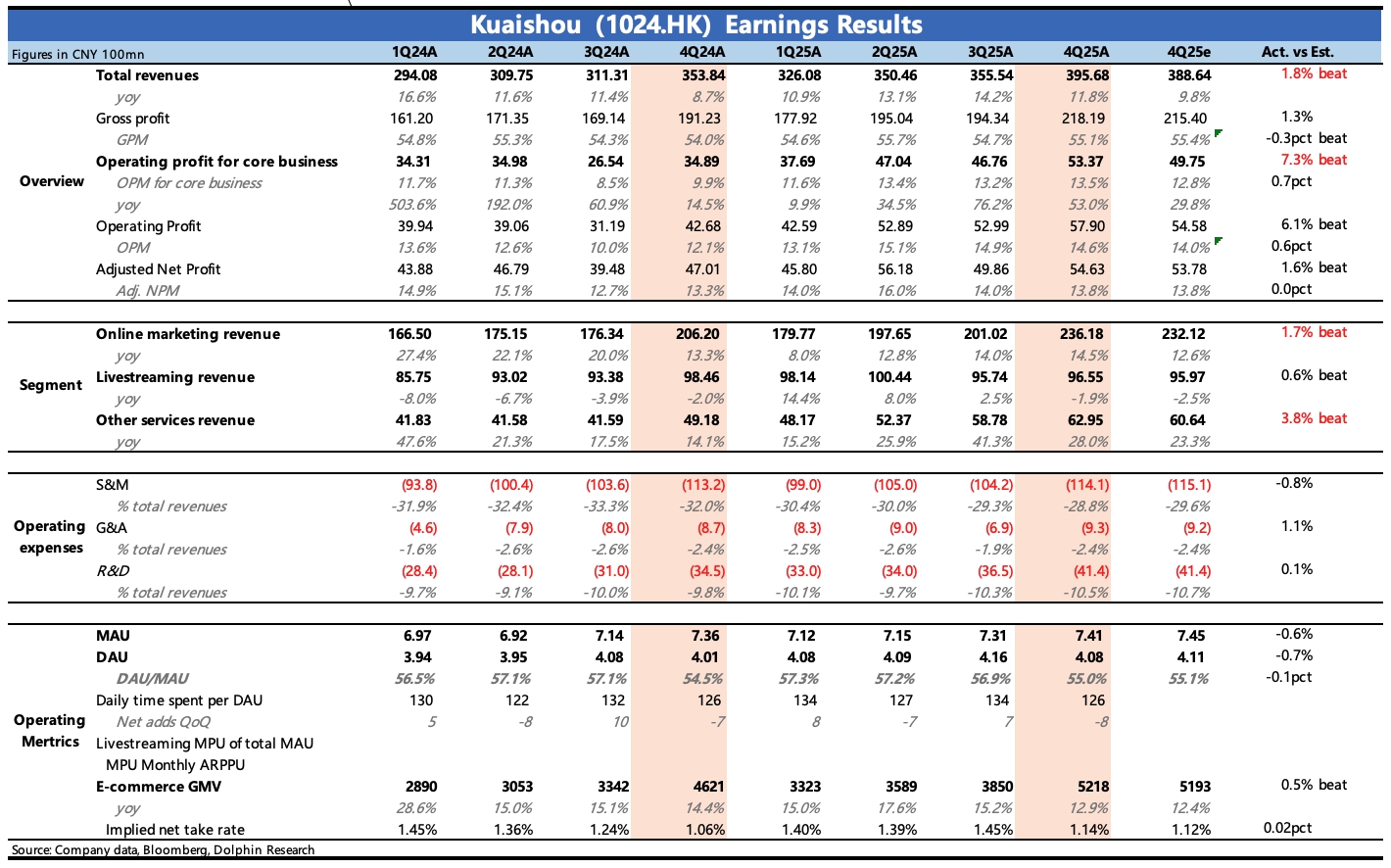

Kuaishou 4Q25 First Take: Q4 came in slightly ahead of expectations, with the upside driven more by tighter opex and better profitability.

By revenue mix, the beat was in legacy ads and e-comm, while Kling marginally missed early-year buy-side expectations and thus did less for the valuation story.

With the stock now at under 9x PE, this negative is likely priced in after the recent pullback.

Guidance on Kling’s growth on the call will be key, as it will determine the rebound potential for a stock currently valued largely on its traditional businesses.

1) Kling fell short of early-year expectations: Kling v2.6 launched in Dec., and thanks to better motion control and synchronized audio-video features, user feedback was strong with monthly gross billings hitting a record of 20mn.

On that, buy-side raised Q4 revenue expectations from the guided 300mn to 350–400mn, and for 2026 to nearly 2bn, implying an almost doubling. These were optimistic assumptions.

Actual Q4 revenue was 340mn, near the low end of guidance and market expectations.

There was likely some preview communication with investors; after a Dec. spike, metrics slipped quickly in Jan., and while Kling 3.0 arrived in Feb., the viral breakout of Seedance 2.0 dampened Kling’s rebound. As a result, expectations were cut, weighing on the share price since Feb.

2) E-comm growth steady: Q4 e-comm GMV rose 13%, with nearly 1.6tn for the full year.

With influencer distribution, full custody, and the Super Link service, the commission take rate improved by 8bps YoY (down QoQ on peak-season rebate accruals). This drove e-comm revenue growth of roughly 22% YoY, slightly ahead of top-house estimates (~18%).

3) Ads slightly beat: Revenue grew 15%, helped by last year’s low base, solid e-comm, the continuing boom in short dramas (incl. AI comics) and mini-games, and incremental adoption of AIGC ad tools.

Ad growth re-accelerated QoQ in Q4.

4) Margin expansion continued: Despite stepping up AI spend (equipment depreciation +10% YoY; R&D +34% YoY), the company tightened basic opex, with staff costs up 4% and S&M flat YoY.

Core OPM reached 13.5%, up 350bps YoY and 40bps QoQ.

5) User ecosystem stable: The platform is mature, so user metrics were steady.

MAU was 740mn, DAU 410mn, user stickiness 55%, and time spent was flat YoY.

6) Potential for higher shareholder returns: With the Q4 correction, the company stepped up buybacks, repurchasing HKD 3.2bn for the full year and announcing a HKD 3.0bn dividend, implying a 2.7% shareholder return.

Kuaishou has ample cash and the stock remains under pressure, so it may maintain sizable buybacks after the blackout; watch management’s commentary on the call. $KUAISHOU-W(01024.HK) $KUAISHOU-WR(81024.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.