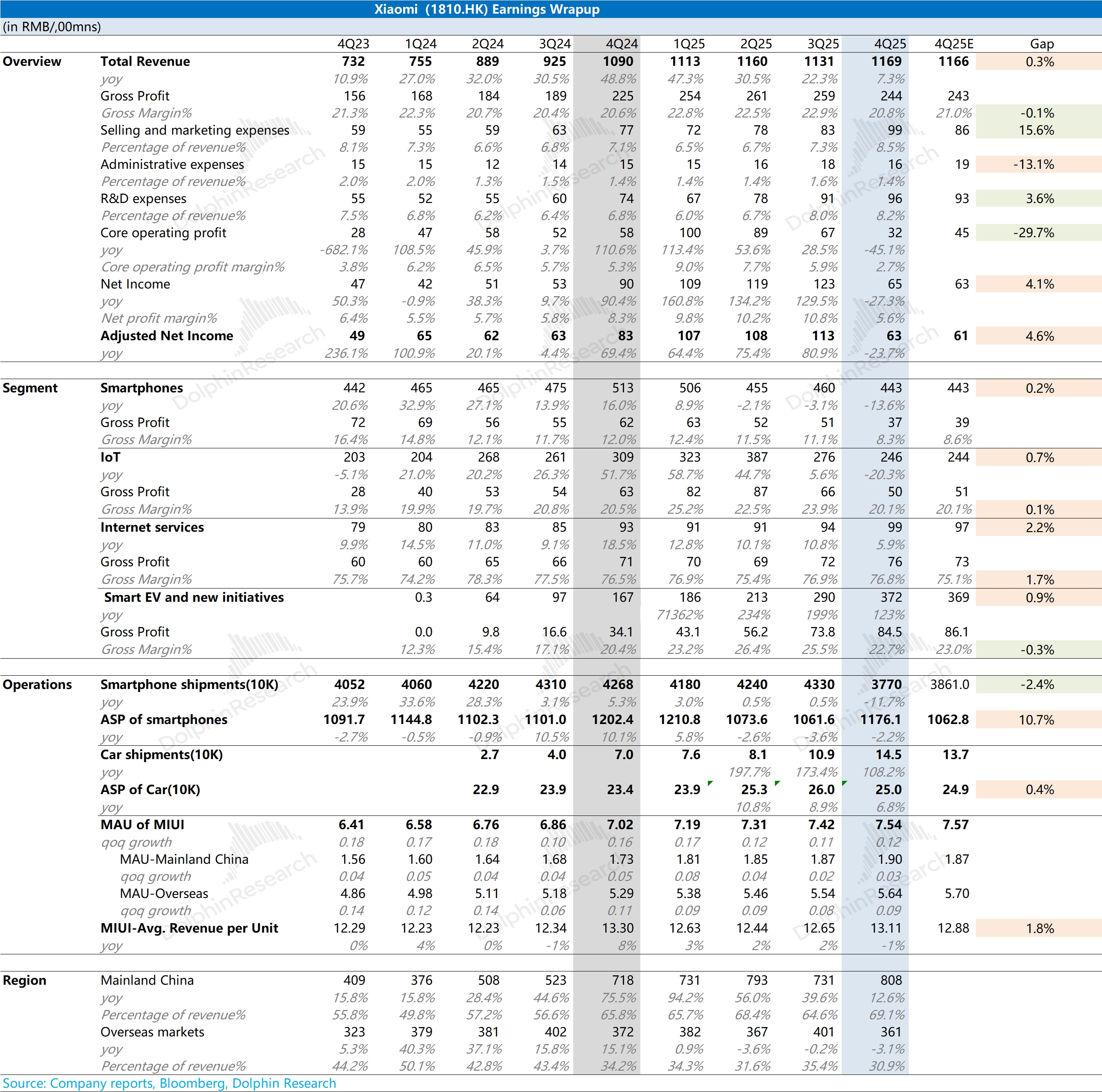

Xiaomi 4Q25 First Take: results broadly in line with our preview. All revenue growth this quarter came from autos, while legacy segments—smartphones and IoT—were under pressure.

This quarter’s prints point to mounting pressure. Smartphone GPM fell to single digits (8.3%), and IoT revenue declined double digits (-20% YoY). Auto GPM also contracted, with weekly orders trending down meaningfully.

With memory prices still rising, a turnaround in smartphones and IoT looks unlikely, and expectations are low. As for autos, after the YU7 cooled, weekly orders deteriorated, falling to around 4k by early Mar.

With legacy businesses soft, autos will need to carry earnings. The mid-cycle refresh of the new-gen SU7 delivered limited surprises, so investors will look to upcoming models and large-model initiatives for the next set of catalysts. For details, stay tuned for Dolphin Research’s follow-up takes and Trans. $XIAOMI-W(01810.HK) $Xiaomi Corporation(XIACY.US) $XIAOMI-WR(81810.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.