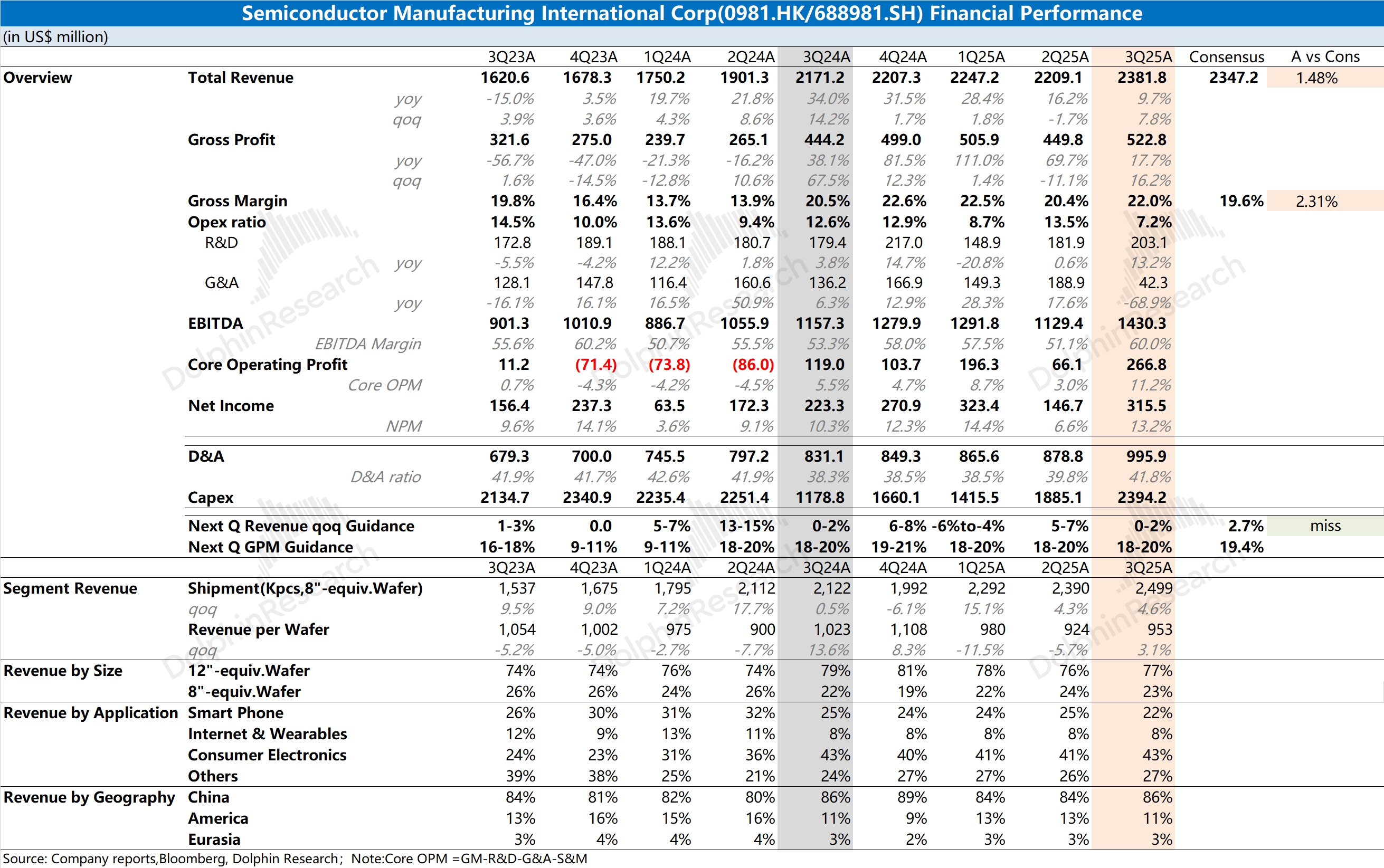

SMIC 3Q25 Quick Interpretation: The company's revenue and gross margin for this quarter exceeded guidance expectations.

The revenue growth was driven by an increase in both wafer shipments and average selling price, with the proportion of 12-inch wafers rising, which contributed to the average price. The increase in average price this quarter was greater than the increase in unit cost, leading to a rise in gross margin.

Although the gross margin improved significantly this quarter, the company's guidance for the next quarter remains quite flat.

The company expects revenue to grow by 0-2% quarter-on-quarter, which is below market expectations (2.7% quarter-on-quarter growth); the company's gross margin guidance for the next quarter remains in the 18-20% range, relatively conservative, but it also suggests that the company may face pressure from increased unit costs next quarter.

Looking at specific business segments: The company's customers are mainly concentrated in China, with domestic revenue accounting for 86%. Among various downstream markets, demand for consumer electronics, industrial and automotive, and smart home has picked up, while the proportion of mobile phone business has fallen back to around 20%.

The company's capital expenditure for this quarter reached $2.39 billion, setting a new quarterly high. The company previously revealed that the full-year capital expenditure for 2025 will be flat compared to 2024, suggesting that fourth-quarter capital expenditure will be $1.64 billion.

Since the fourth quarter often has a significant capital expenditure performance throughout the year, Dolphin Research expects the company's full-year capital expenditure to exceed last year's $7.33 billion.

Overall, although the traditional semiconductor industry has not truly recovered, SMIC still maintains a high level of capital expenditure and expansion pace.

Although the company's gross margin is only around 20%, lower than peers like UMC and GlobalFoundries, the company enjoys a higher valuation level, mainly due to the long-term belief in the company's continuous growth and process breakthroughs.

In the current situation, as long as the company continues to maintain high capital investment and steady expansion, short-term performance disturbances will not affect investors' "long-term confidence."

Whenever technological friction, geopolitical risks, and other factors escalate, the value of the company and the local supply chain will further manifest. For more information, please follow Dolphin Research's subsequent commentary and management communication minutes. $SMIC(00981.HK) $SMIC(688981.SH)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.