$Li Auto(LI.US) Quick Interpretation: Overall, Li Auto's performance this time is very important from two dimensions: ① Actual performance in Q4 2024, ② Guidance for Q1 2025.

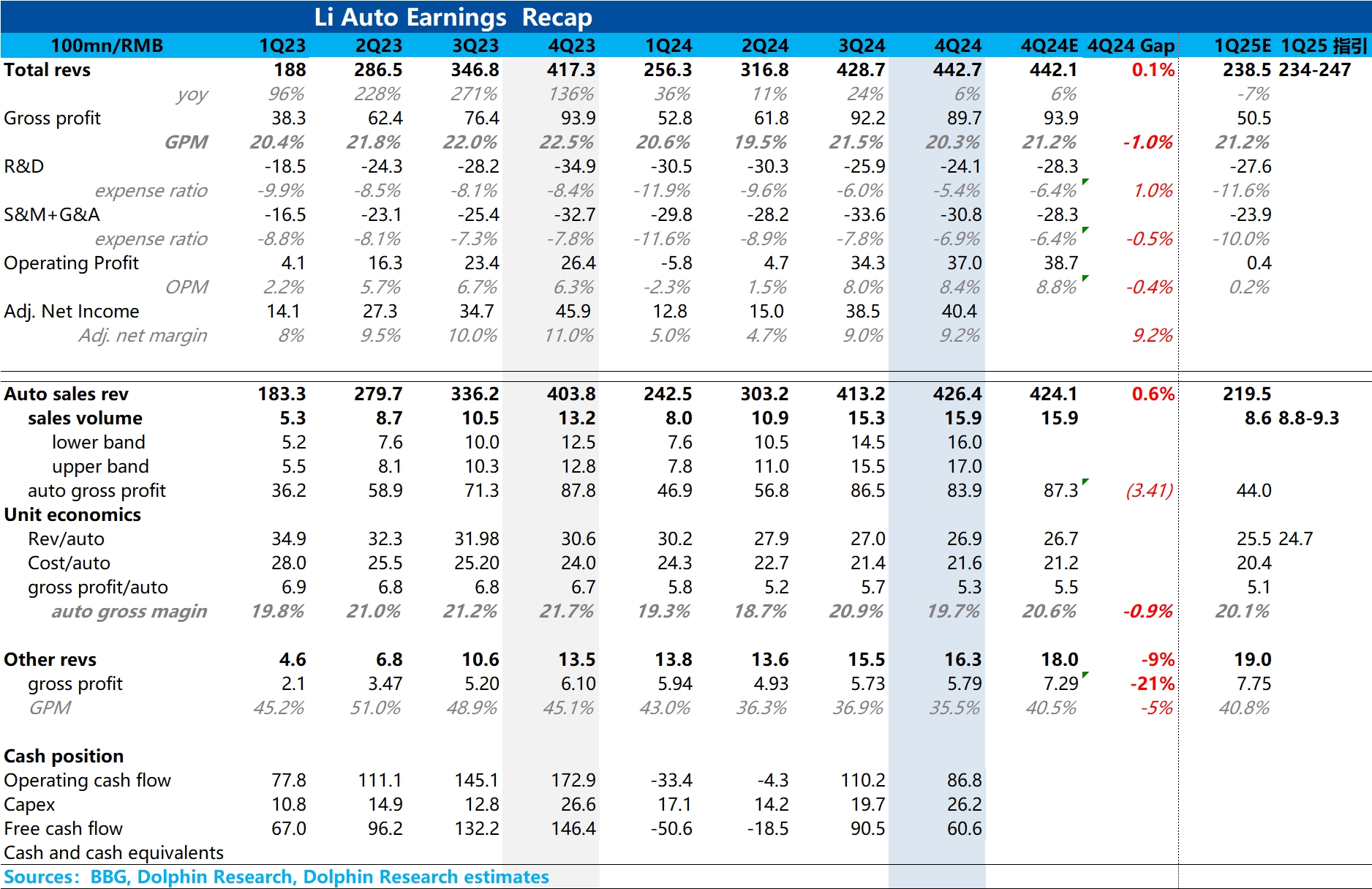

From the actual performance in Q4 2024, the most critical automotive gross margin missed market expectations, with the gross margin for automotive business only at 19.7% this quarter, a decrease of 1.2 percentage points quarter-on-quarter, while the market consensus expectation was still at 20.6%, and major institutions even expected it to reach 21.3%.

However, considering that the actual automotive business gross margin in Q3 2024 included a rebate from CATL, the actual automotive business gross margin in the third quarter was 19.5%. Although there was no one-time factor of battery rebates confirmed in the fourth quarter, Li Auto did guide for a gross margin of over 20% for the automotive business in Q4 2024, mainly contributed by annual reductions from suppliers and scale effects. However, it is clear that when the scale effect has not been released (the delivery volume in Q4 was lower than Li Auto's guidance for Q3), the annual reductions from suppliers also did not meet expectations.

From the perspective of operating profit and net profit, operating profit did indeed improve quarter-on-quarter compared to Q3, but mainly due to the confirmation of a large amount of SBC (related to the CEO's reward for every 500,000 milestone in sales) in Q3. In Q4, the SBC alone was about 500 million less than in Q3 2024, so after excluding the impact of SBC changes, the operating profit in Q4 2024 decreased compared to Q3 (a decrease of 200 million), which also did not meet market expectations.

As for the guidance for Q1 2025, ① Sales guidance is 88,000 to 93,000 units, implying March sales of 32,000 to 37,000 units, an increase of 5,500 to 10,500 units compared to February. It can be seen that the price reduction in March indeed had an effect, and this guidance is acceptable; ② However, in terms of unit price guidance (the implied unit price guidance from revenue guidance), the unit price in Q1 2025 has dropped significantly, decreasing by nearly 22,000 to 247,000, still mainly due to the impact of the price reduction in March, and the expected automotive gross margin may not be good either, with specifics likely to wait for information from Li Auto's conference call.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.