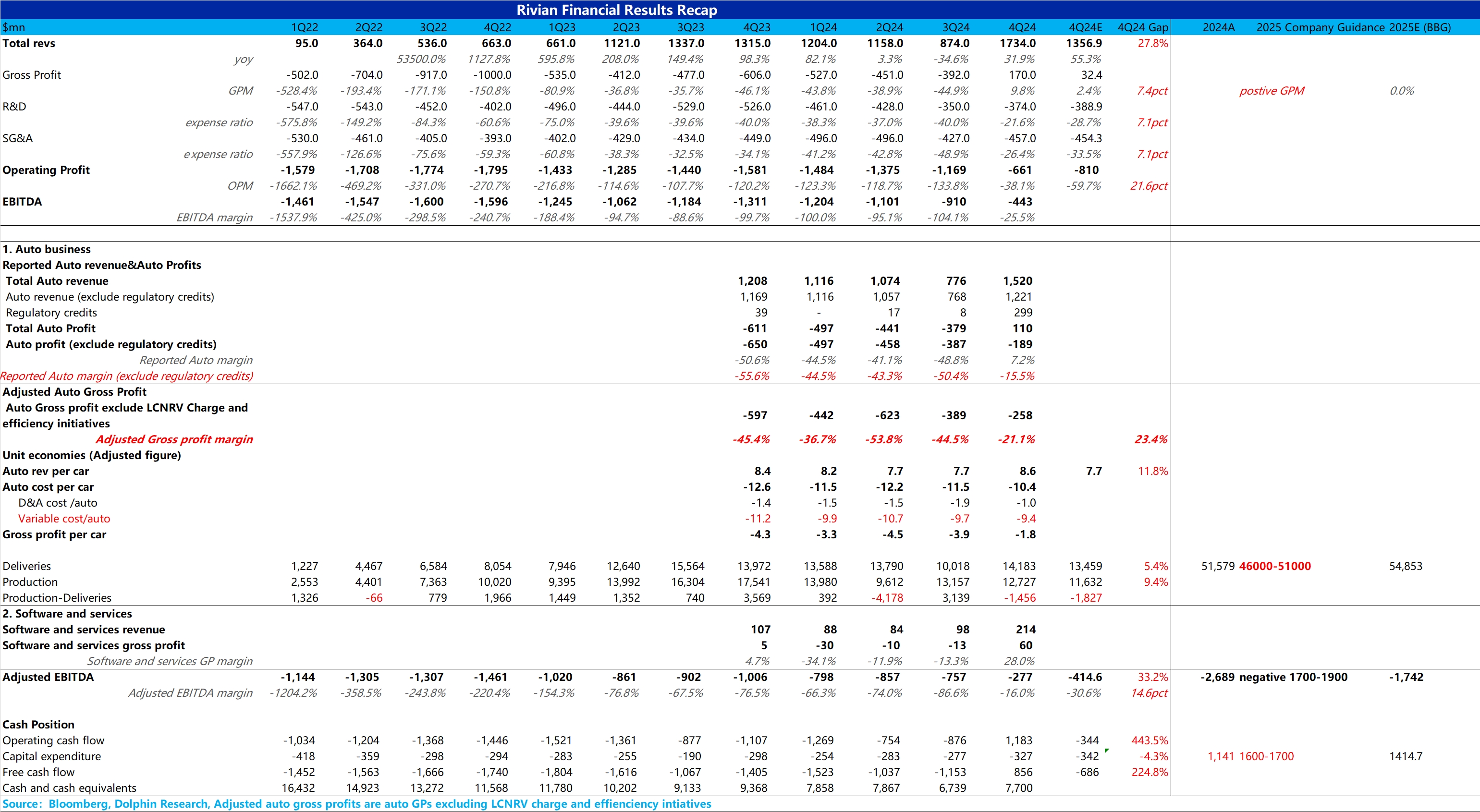

$Rivian Automotive(RIVN.US) Earnings Quick Interpretation: Overall, the fourth-quarter performance exceeded expectations across the board. More importantly, as the company repeatedly emphasized, the gross margin on the financial statements successfully turned positive, even reaching 9.8%, which was 2.4% higher than the market consensus.

Due to the relatively large adjustments in Rivian's financial statements this time, the market is most concerned about the performance of Rivian's core automotive business. Dolphin Research has broken down the earnings to analyze the automotive business separately.

From the perspective of the automotive business, the gross margin for the automotive segment on the financial statements successfully turned positive (7.2%) this quarter. However, this was largely due to a significant regulatory credit income recognized in Q4 2024 (consistent with management's guidance last quarter). Excluding this regulatory credit, the automotive business gross margin was -15.5%. Although it still hasn't turned positive, it improved by 35 percentage points compared to the previous quarter, which is a significant improvement.

However, the automotive gross margin on the financial statements was also affected by inventory and contract impairment reversals, as well as one-time cost factors. Since the amount of inventory and contract impairment reversals in 2025 will be minimal, and the one-time costs (mainly related to the second-generation R1 update) are unlikely to recur in 2025, Dolphin Research excluded these two factors to observe the true automotive business gross margin. From the true automotive business gross margin this quarter (also excluding regulatory credits), there was still a notable improvement. The true automotive business gross margin in Q4 was -21.1%, up 23 percentage points quarter-over-quarter.

The core reasons for the quarter-over-quarter improvement:

① The most significant factor: The average revenue per vehicle in Q4 was $86,000, up $9,400 quarter-over-quarter, far exceeding the market's expectation of flat revenue per vehicle. The increase in revenue per vehicle was mainly due to: a. This quarter primarily involved deliveries of the latest R1 model, which generally did not offer discounts, whereas Q2 and Q3 still involved significant deliveries of older inventory (pre-update R1 versions with substantial discounts); b. The sales mix included the introduction of the tri-motor R1 (a more expensive version), boosting the average selling price (ASP), though this was partially offset by the increased proportion of EDV (commercial vans with lower unit prices).

② The second factor: The average depreciation cost per vehicle decreased by $8,000 quarter-over-quarter, partly due to economies of scale but mainly because the company accelerated depreciation for the second-generation R1 upgrade in Q2-Q3 and improved factory operational efficiency.

③ However, the most critical point is the reduction in variable costs, which is the market's primary concern. Recall that Rivian repeatedly emphasized that the R1 upgrade involved replacing 50% of suppliers, leading to a significant reduction in BOM costs (Rivian previously expected a 20% reduction in BOM costs from Q1 2024 to Q4 2024).

However, the reduction in variable costs this quarter was modest, declining by less than $3,000 quarter-over-quarter and only $5,000 compared to Q1. Additionally, this quarter benefited from the contribution of the lower-cost, higher-margin EDV, leading investors to question whether the cost reduction for the second-generation R1 was as significant as the company had guided.

Combined with the lower-than-expected delivery guidance for 2025 (only 46,000-51,000 units, below the market expectation of 55,000 units and even below the actual 2024 deliveries of 51,600 units), this implies weak demand for the R1. The market is also concerned that the increased revenue per vehicle this quarter may not be sustainable and could continue to decline.

Given the underwhelming cost reductions, it's foreseeable that the true automotive business gross margin expectations for 2025 may not be favorable, and the improvement trend seen in Q4 2024 may not persist. For a detailed analysis, please refer to Dolphin Research's upcoming commentary.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.