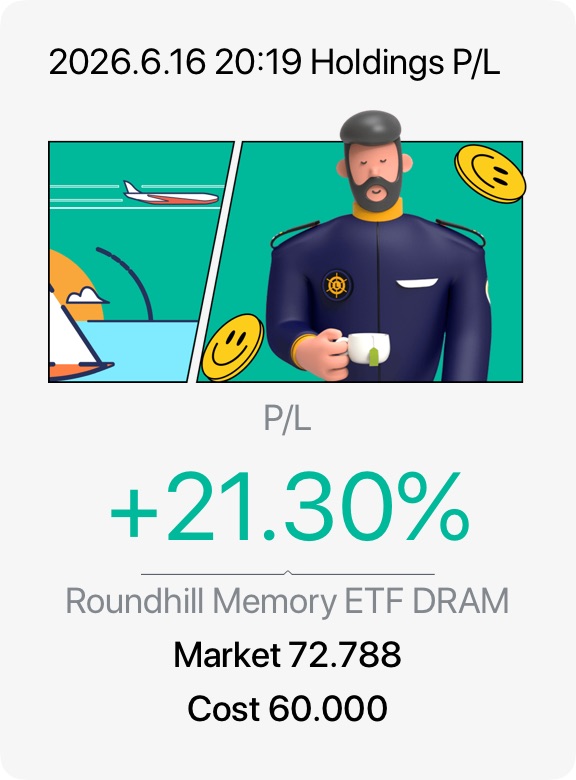

$Roundhill Memory ETF(DRAM.US)prices have seen massive increases driven primarily by AI demand, with contract prices nearly doubling in Q1 and further significant rises expected in Q2. The pace of monthly increases has slowed recently in retail/spot markets, but overall levels remain highly elevated, and supply tightness is expected to persist through the rest of 2026.

The core cause is the AI supercycle:

Explosive demand for HBM (High Bandwidth Memory), a premium DRAM type, and high-capacity/high-density conventional DDR5 for AI servers and data centers.

Major producers (Samsung, SK Hynix, Micron) are reallocating wafer capacity and prioritizing high-margin server/AI products (including HBM and high-capacity RDIMMs) over standard DRAM used in PCs, smartphones, and industrial applications.

HBM is expected to account for ~25% of total DRAM wafer production in 2026, with demand growing ~70% YoY. This effectively displaces supply for everyday DRAM.

Low supplier inventories, allocation controls, and long lead times (often 30–40+ weeks) exacerbate shortages.

Hyperscalers (cloud/AI giants) are locking in supply via multi-year deals and accepting higher prices, which cascades to other buyers.

@Bridge Buzz SG

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.