$Lululemon(LULU.US)

🚨 Lululemon 1Q 2026 Earnings: A Tale of Two Realities

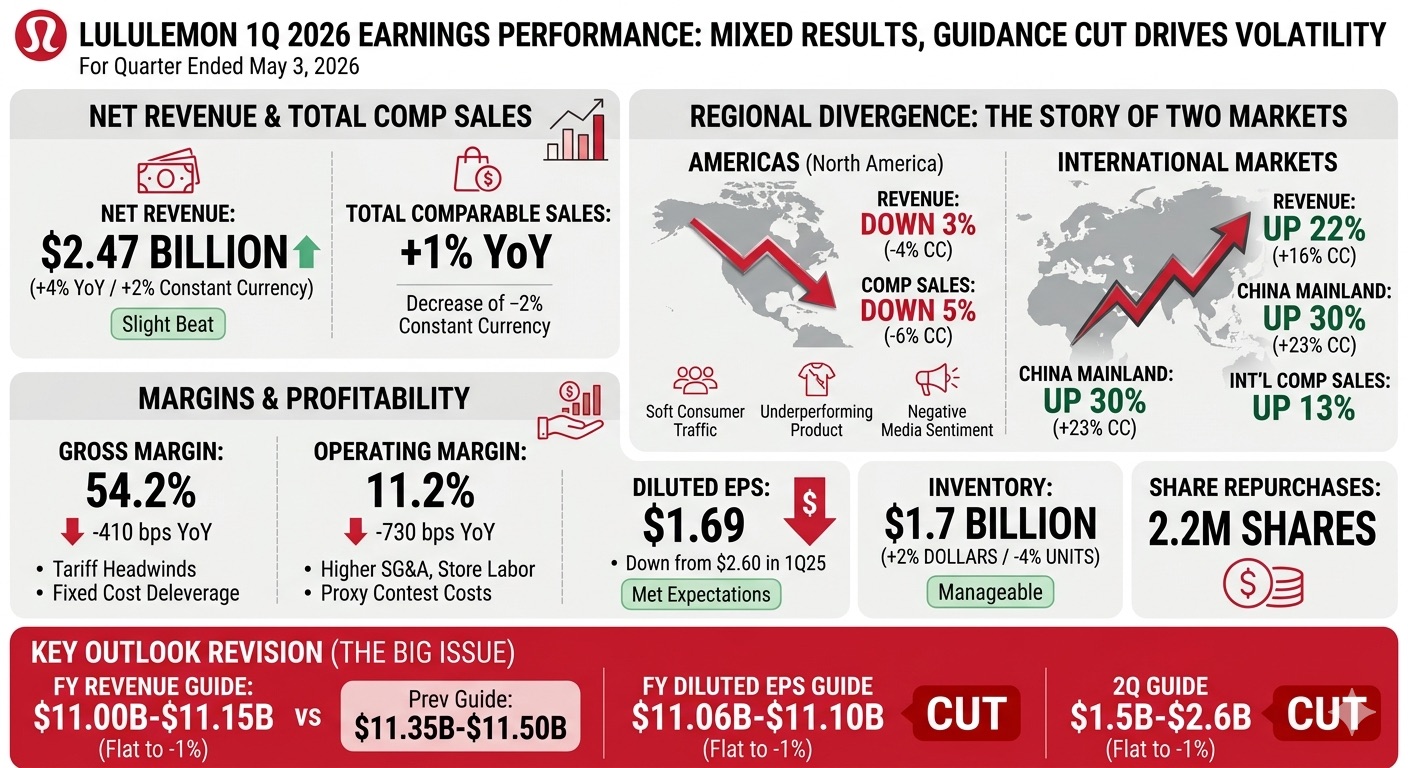

LULU just dropped its latest quarterly results and it is a highly mixed bag! The top-line revenue managed a slight beat, a severe outlook downgrade for the rest of the year has sparked massive market volatility.

Here is the quick breakdown of the core numbers you need to know:

🟢The Top-Line: Net revenue ticked up 4% to $2.47 billion (a slight beat), but total comparable sales slowed to just +1% YoY.

🟢The Regional Split: A stark contrast in growth engines. Americas revenue fell 3% (with comps down 5%) due to soft traffic and product misses. Meanwhile, International surged 22%, powered by a massive 30% explosion in Mainland China!

🟢Margin Squeeze: Profitability took a hit. Gross margin contracted 410 bps to 54.2% under the weight of global tariffs, while operating margin fell to 11.2% on higher SG&A and labor costs.

🟢The Bottom Line: Diluted EPS came in at $1.69 (down from $2.60 last year), narrowly meeting lowered expectations.

🟢The Big Issue: Management sharply cut full-year 2026 guidance, dropping expected FY revenue to $11.00B–$11.15B and EPS to $10.95–$11.15.

🎨 Want a quick visual breakdown? I have prepared a handy infographic below for your easy reading!

What are your thoughts on LULU’s growth pivot to China? Let’s discuss👇

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.