中芯国际 2025 年第一季度

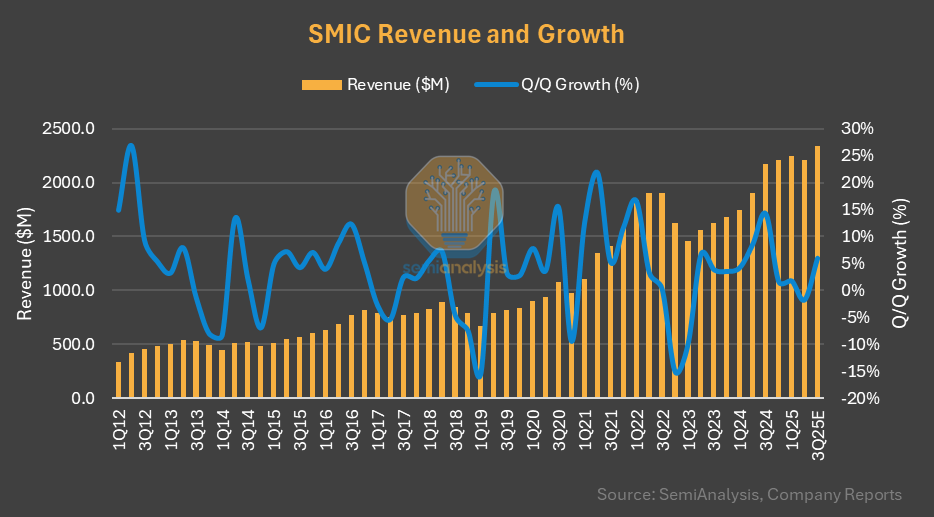

- 收入环比下降 2%,同比下降 16%,至 22 亿美元(优于预期的 4% 至 6% 下降);连续七个季度同比增长;9 月季度也将增长- 晶圆出货量(300 毫米等效):106.2 万片(环比增长 4%)- 晶圆平均售价:1967 美元(环比下降 6%)- 产能利用率:92.5%(对比 2025 年第一季度的 89.6%)- 2025 年资本支出预计与 2024 年相似(70 亿美元以上)来源:Sravan Kundojjala

本文版权归属原作者/机构所有。

当前内容仅代表作者观点,与本平台立场无关。内容仅供投资者参考,亦不构成任何投资建议。如对本平台提供的内容服务有任何疑问或建议,请联系我们。

发表你的评论

暂无评论