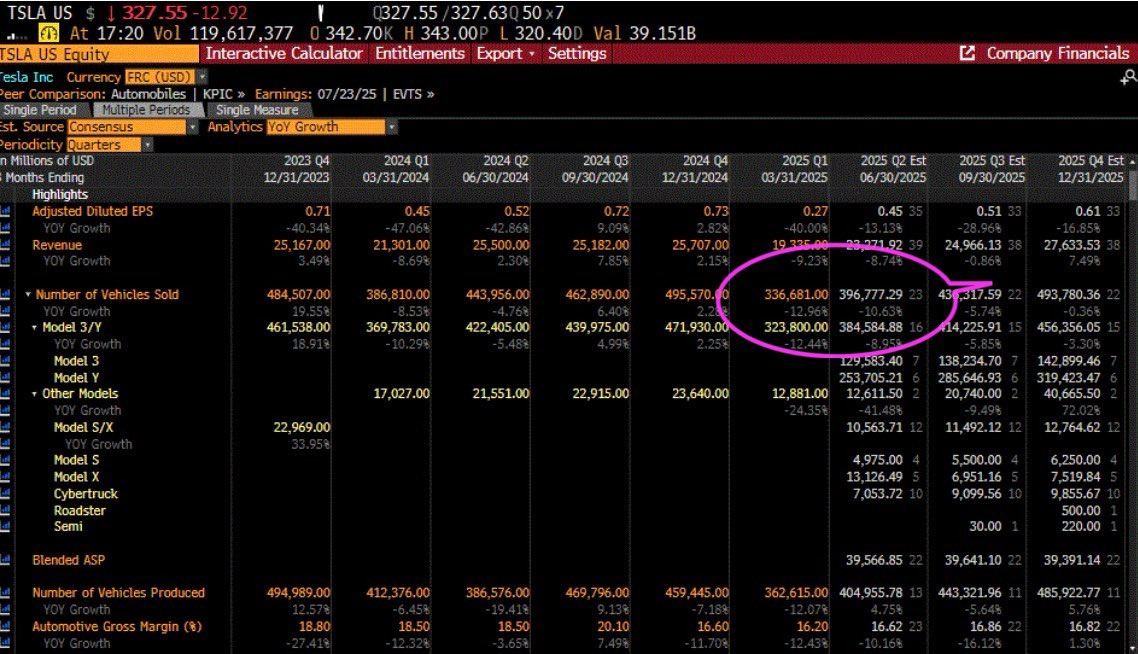

$特斯拉(TSLA.US) 的下一个催化剂是下周三 7 月 2 日的第二季度交付数据。我们现在预测第二季度交付量为 37.5 万辆,同比下降 16%,而华尔街共识预期为 39.7 万辆,同比下降 11%。这一同比下降幅度将比 4 月 2 日报告的 337,000 辆(同比下降 13%)更糟糕。

尽管许多投资者认为,鉴于 Robotaxi 的重要性和规模扩大,电动汽车交付量已不再重要,但我们目前预计 2025 财年 TSLA 的交付量将同比下降 10% 至 161 万辆(华尔街预期为 167.6 万辆,同比下降 6%),这可能会导致进一步的每股收益下调(2025 财年调整后每股收益目前为 1.88 美元,同比下降 42%)。我们预计第三季度推出的更便宜的特斯拉将是现有 Model Y 的低成本版本,而不是新的车型(例如掀背车),我们预计这将增加很少或没有增量交付量。

本文版权归属原作者/机构所有。

当前内容仅代表作者观点,与本平台立场无关。内容仅供投资者参考,亦不构成任何投资建议。如对本平台提供的内容服务有任何疑问或建议,请联系我们。

发表你的评论

暂无评论