China Mobile's third-quarter revenue increased by 2.5% year-on-year, with AI direct revenue achieving rapid growth | Financial Report Insights

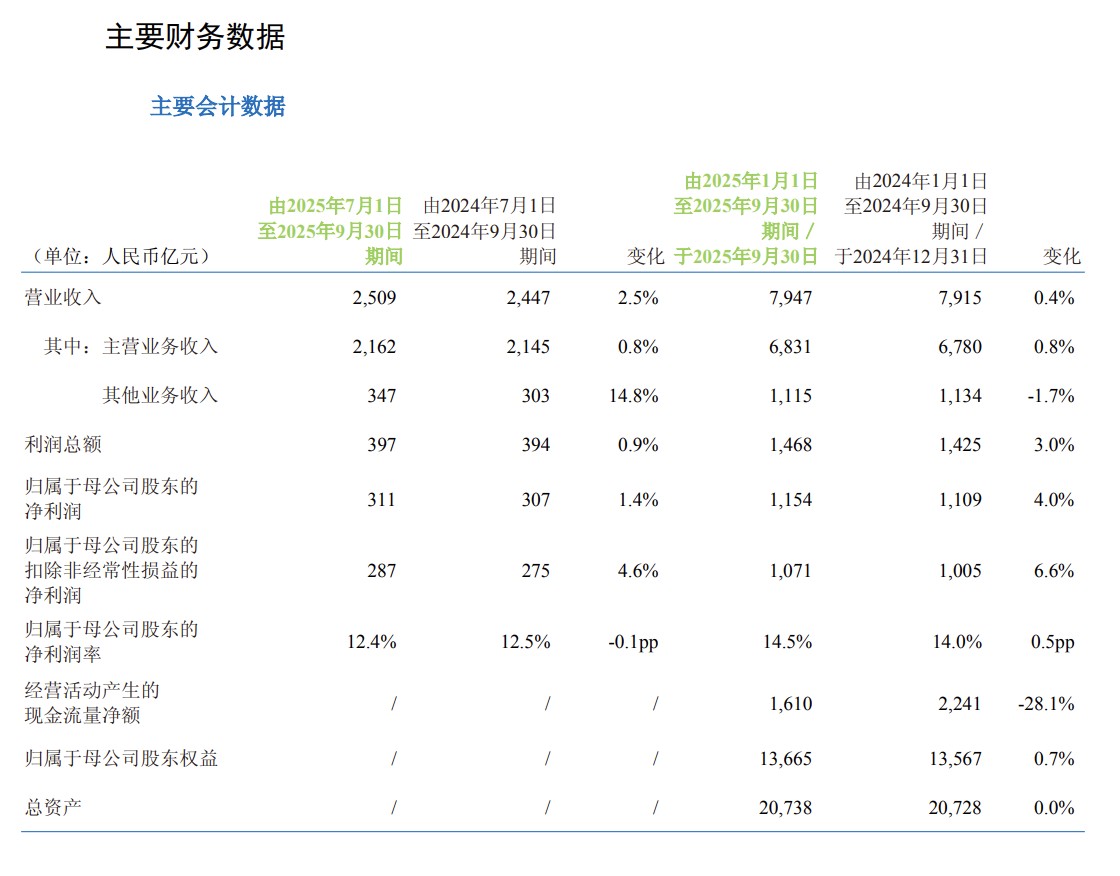

China Mobile's revenue for the third quarter was CNY 250.9 billion, a year-on-year increase of 2.5%, with an improved growth rate compared to the previous quarter. The net profit margin attributable to the parent company increased to 14.5%, up 0.5 percentage points year-on-year. Among them, the DICT business maintained good growth, AI direct revenue achieved rapid growth, and international business continued to grow rapidly

China Mobile delivered a "mediocre" performance in the third quarter. In the first three quarters, operating revenue was CNY 794.7 billion, a year-on-year increase of only 0.4%, highlighting the weak growth of traditional businesses. However, looking at the single quarter, third-quarter revenue was CNY 250.9 billion, a year-on-year increase of 2.5%, showing improvement compared to the previous two quarters, indicating a marginally better operating environment.

On Monday, China Mobile released its third-quarter financial report, specifically:

- Financial performance: Operating revenue for the first three quarters was CNY 794.7 billion, a slight increase of 0.4% year-on-year; net profit attributable to the parent company was CNY 115.4 billion, a year-on-year increase of 4.0%; third-quarter single-quarter revenue was CNY 250.9 billion, a year-on-year increase of 2.5%, with improved growth compared to previous quarters.

- Profitability: Net profit margin attributable to the parent company increased to 14.5%, up 0.5 percentage points year-on-year; EBITDA was CNY 265.4 billion, a year-on-year increase of 0.9%, with EBITDA margin remaining flat at 33.4%, while the Q3 single-quarter EBITDA margin decreased by 1.3 percentage points to 31.7%.

- Cash flow pressure: Operating cash flow net amount for the first three quarters was CNY 161.0 billion, a significant year-on-year decrease of 28.1%, dropping over CNY 60 billion from CNY 224.1 billion, indicating capital expenditure pressure.

- User growth: 5G network customers reached 622 million, a net increase of 23 million; total mobile customers reached 1.009 billion; broadband customers reached 329 million, a net increase of 14.2 million.

- Business highlights: DICT business maintained good growth, AI direct revenue achieved rapid growth, and international business continued to grow rapidly

Q3 Revenue Improved Sequentially

China Mobile's operating revenue for the first three quarters was CNY 794.7 billion, with a year-on-year growth rate of only 0.4%, nearly stagnating. Notably, Q3 single-quarter operating revenue was CNY 250.9 billion, a year-on-year increase of 2.5%, showing sequential improvement.

Main business revenue grew by 0.8% to CNY 683.1 billion, which is also weak. Traditional mobile business faces pressure: Q3 mobile ARPU dropped to CNY 48.0 per user per month, down CNY 1.5 from Q2's CNY 49.5, a decline of 3%. Although mobile internet DOU increased to 17.0GB, a year-on-year increase of 8.1%, the continuous dilution of traffic value has clearly dragged down revenue performance. The total number of mobile customers reached 1.009 billion, with 5G users at 622 million; the slight increase in user scale could not offset the impact of declining ARPU.

Against the backdrop of weak revenue growth, net profit attributable to the parent company was CNY 115.4 billion, a year-on-year increase of 4.0%, with net profit margin rising to 14.5%. Specifically, non-recurring gains and losses contributed CNY 8.25 billion, with fair value changes and disposal gains of financial assets reaching CNY 8.08 billion, accounting for a significant proportion.

After deducting non-recurring gains and losses, net profit was CNY 107.1 billion, a year-on-year increase of 6.6%, which is even more robust, indicating that the company's main business profitability has indeed improved. Cost control is a key factor: operating costs were CNY 547.6 billion, basically flat compared to the same period last year, with both selling expenses and management expenses decreasing, showing significant expense control effects However, the Q3 single-quarter EBITDA margin was 31.7%, a year-on-year decline of 1.3 percentage points, indicating pressure on operating profit margins. Although the full-year EBITDA margin remained at 33.4%, the quarterly fluctuations are concerning and may be related to the pace of capital expenditures and depreciation and amortization pressures.

Significant Decline in Cash Flow

The most concerning issue is the deterioration of cash flow. In the first three quarters, the net operating cash flow was 161 billion yuan, a year-on-year plunge of 28.1%, down 63.1 billion yuan from 224.1 billion yuan in the same period last year. This figure sharply contrasts with the growth in net profit, reflecting the company's pressure in managing working capital such as accounts receivable and inventory.

The financial statements show that accounts receivable surged from 75.7 billion yuan at the beginning of the year to 111.5 billion yuan, an increase of 47%, which may be related to the expansion of government and enterprise business and extended payment terms. Meanwhile, cash paid for purchasing goods and receiving services reached 492.6 billion yuan, a year-on-year increase of 7.8%, far exceeding revenue growth, further squeezing cash flow.

In terms of investment activities, cash payments for the purchase of fixed assets and other long-term assets amounted to 117.1 billion yuan, roughly flat compared to last year, but cash payments for investments reached 75.5 billion yuan, a year-on-year increase of 21%, indicating the company's continued investment in areas such as 5G networks and computing infrastructure. Monetary funds decreased from 242.3 billion yuan at the beginning of the year to 161.1 billion yuan, a reduction of 81.2 billion yuan, a decline of 33.5%, narrowing financial flexibility.

DICT and AI as Growth Engines

Against the backdrop of pressure on traditional businesses, the company is actively cultivating new growth points. DICT business revenue has maintained good growth, and AI direct revenue has achieved rapid growth. Although the financial report did not disclose specific data, from the strategic statements, the government and enterprise market is becoming a new value growth pole.

International business also performed well, with rapid growth in international business revenue in the first three quarters. The company is seizing high-level opening-up opportunities and leveraging the synergy between domestic and international markets. In terms of content business, through "content + technology + integrated innovation" operations, the scale of key product customers has achieved steady growth.

Expectation Gaps and Future Highlights

China Mobile's performance in the first three quarters shows typical transformation characteristics: traditional business growth is weak, user value continues to dilute, and cash flow pressure is increasing, but emerging businesses are beginning to show vitality, cost control is effective, and profit margins are steadily improving.

In the future, several aspects need to be closely monitored: first, whether the ARPU value can stabilize, which relates to whether sustainable growth can be achieved on the revenue side; second, the balance between capital expenditure scale and cash flow, whether sustained high-intensity investment can be converted into revenue growth; third, the profitability of emerging businesses such as DICT and AI, whether they can become new profit growth points; fourth, the commercialization path after the increase in 5G penetration rate, how to convert network advantages into revenue advantages