Before the end of the year, will there be at least one 50 basis point rate cut among "two rate cuts"? The options market bets that the Federal Reserve will "do more"

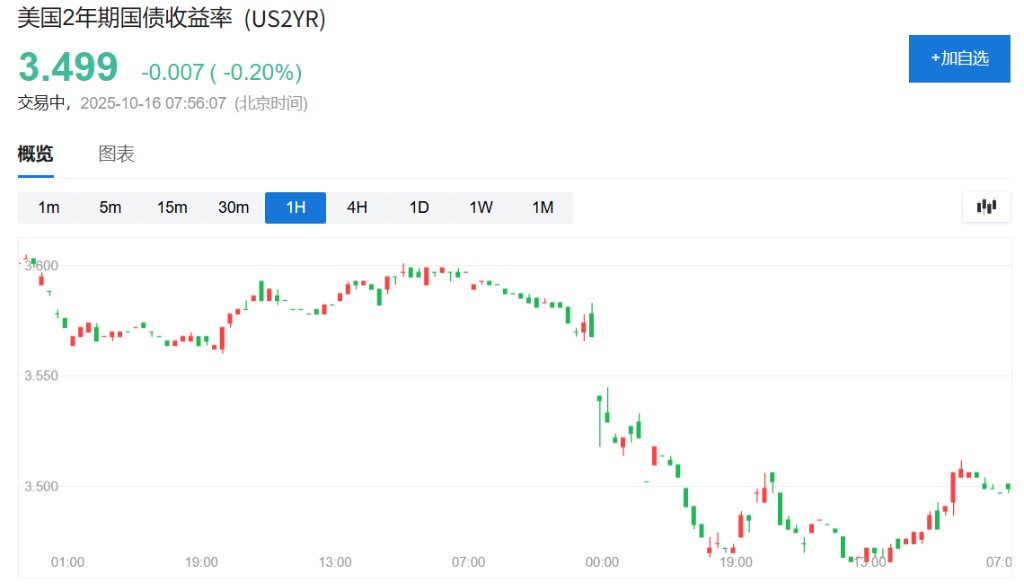

Recently, the options market linked to the Secured Overnight Financing Rate (SOFR) shows that traders are positioning for a 50 basis point rate cut by the Federal Reserve at the October or December meeting. Open interest in December SOFR options has surged significantly. This bullish sentiment is also reflected in the spot market, where the yield on the two-year U.S. Treasury bond has recently fallen to around 3.5%, a year-to-date low

Options market traders are betting that the Federal Reserve will implement at least one significant 50 basis point rate cut before the end of the year, a more aggressive expectation than the current pricing in the interest rate swap market for two 25 basis point cuts.

Recent options market activity linked to the Secured Overnight Financing Rate (SOFR) shows that traders are positioning for a 50 basis point rate cut at the Fed's October or December meetings.

Open interest in December SOFR options has surged significantly, as these options expire two days after the policy announcement on December 10, making them an ideal tool for betting on the direction of policy in the remaining two meetings of the year. This bullish sentiment is also reflected in the spot market, where the yield on the two-year U.S. Treasury recently fell to around 3.5%, a year-to-date low.

Despite the U.S. government shutdown delaying the release of key data such as employment figures for several weeks, the market expects that once the government reopens, a wealth of economic data will provide more evidence of economic weakness, thereby supporting further rate cuts.

Options Bets Focused on Significant Year-End Rate Cuts

The options market serves as an important window into traders' expectations, and recent signs clearly point to bets on the Fed taking more aggressive action.

There has been a noticeable buying interest in options linked to December SOFR, with open interest—an indicator of the risk held by traders—sharply rising. Since these options expire two days after the Fed's policy statement on December 10, they have become the ideal tool for betting on the policy direction in the remaining two meetings of the year.

This week's trading has continued the trend from last week, with traders buying various options structures aimed at hedging a "dovish scenario" (such as a 50 basis point cut).

Specific trading flows indicate that funds have purchased call spread combinations of 96.50/96.5625 and 96.50/96.625, with buyers also acquiring a call spread combination of 96.5625/96.75 on Monday. These trading flows all point to the possibility of a 50 basis point cut at the October or December meetings.

To understand these bets, it is essential to first grasp SOFR. SOFR (Secured Overnight Financing Rate) is a key rate that reflects the cost of overnight borrowing secured by U.S. Treasury securities. Because it is based on real transactions in the trillions of dollars daily and is backed by Treasuries, its credit risk is extremely low.

SOFR options are financial derivatives based on SOFR interest rate futures. In simple terms, traders buy and sell SOFR options to bet on the future direction of short-term interest rates. The price of interest rate futures moves inversely to the interest rates themselves; a rising price indicates that the market expects rates to fall.

Therefore, when traders aggressively buy SOFR call options, they are essentially betting that the Fed will cut rates. Betting on a series of high strike call options suggests they believe the magnitude of the cuts could be substantial.

Multiple Indicators Show Dovish Tendencies

In addition to the SOFR options market, several other market indicators also reflect investors' dovish tendencies.

According to JP Morgan's client survey for the week ending October 14, the proportion of investors holding neutral positions rose to a one-month high, while short positions decreased by 4 percentage points, indicating that the market's willingness to short interest rates (i.e., bet on rate hikes) is weakening.

In the U.S. Treasury options market, the premium of call options used to hedge against rising prices of 10-year Treasury futures (i.e., falling yields) has risen to its highest level since April relative to put options.

This indicates that traders are willing to pay a higher cost to guard against the risk of a rebound in the bond market due to expectations of interest rate cuts. John Madziyire, a portfolio manager at Vanguard, stated:

Considering the balance of risks, you do want to have a slight inclination towards being long